One of my favorite generative AI/AGI writers is Professor Ethan Mollick, whose latest book is “Co-Intelligence: Living and Working with AI” and who is also the author of the substack One Useful Thing. As someone with early access to the latest frontier models from labs including Open AI and Anthropic, he’s one of my first reads when the latest models are released so that I can quickly be up to speed on the advancements and new capabilities. And while Professor Mollick finds AI remarkable and shares compelling use cases for the technology, he also talks about “the jagged frontier”. The jagged frontier is a concept that describes the uneven and unpredictable boundaries of AI capability. In essence, AI can perform complex, expert-level tasks, such as math and coding, with remarkable efficiency and efficacy, while failing at seemingly simpler tasks that lie outside the capability reach of the models. In his GPT-5.5 post, he mentions that “every few months a new model arrives…[and] the size of the leaps grows each new release cycle. The jagged frontier is still there. It is just much further out than it used to be”.

While I’m very fascinated by AI’s applications, this post will largely not be about AI. Instead I’ll cover my perspective on the current state and where I believe the future of live sports is headed. In short, the compellingness of the offerings, such as new leagues that are launching, continues to grow. And the business models are evolving, providing a more sustainable path for new and emergent leagues, while the cross-device customer experience improves as well, becoming more personalized and immersive. However, while the leagues that are launching have compelling value propositions and the CX continues to improve, I would argue that a jagged frontier remains for live sports. It’s uncertain if the jagged frontier is further out than it used to be, but anyone who argues they know where live sports will ultimately land in five to ten years is likely not exercising the proper humility. From my perspective, the reasons the jagged frontier of live sports remains are a few fold:

- Economics: advertising only/advertising mostly or subscription only/subscription mostly business models are likely not the path to profitable longevity,

- Discovery: customer discovery remains a challenge, even when leagues are available on the largest TV platforms out there, including Roku and Samsung,

- Fragmentation: a customer pain point for every league, from the NFL and NBA down to college sports and below,

- Customer retention: for subscription-based services, churn is an ever-present challenge, that arguably becomes more and more challenging as the proliferation of customer options continues, and

- Engagement share: Competition for engagement and time spent, when you’re competing against behemoths like Netflix, YouTube, and Meta, has never been more challenging and will only get more competitive.

Summary of New and Emergent Leagues

Women’s Sports

- League One Volleyball, LOVB (Jan 2025)

- Model: linear (ESPN, USA Network), free FAST (Victory+, Women’s Sports Network), and subscription (ESPN+)

- Youth club membership base across 77 locations in 28 states

- Major League Volleyball, MLV (2026)

- Model: Linear (CBS Sports) and subscription (Peacock)

- Unrivaled (Jan 2025)

- Model: Linear (TNT, TruTV) and subscription (Max)

- TNT Sports took an equity stake in lieu of a traditional cash rights fee

- PWHL (Jan 2024)

- Model: Free (YouTube, global); linear regional (TSN, CBC, RSNs); subscription (Prime Video, Canada); no US national rights deal yet

- WLL (2025)

- Model: Subscription (ESPN+) and select linear (ABC, ESPN); ESPN made a minority equity investment in parent PLL

- USL Super League (Aug 2024)

- Model: Subscription-only (Peacock exclusive home of all matches)

- Women’s Professional Basketball League, WPBL (2026, planned)

- Model: No media deal announced

- Women’s Elite Rugby, WER (2025)

- Model: No major media deal announced

Primarily Men’s Sports

- TGL (Jan 2025)

- Model: Linear (ESPN primetime)

- AFFL / NFL Flag Football (2026 pro launch)

- Model: No media deal announced

- NFL investing $32M via TMRW Sports-operated professional league

- Major League Cricket (Jul 2023)

- Model: Subscription-first domestic (Willow TV); supplemented by RSN team packages and international broadcast deals

- PBR Team Series (Jun 2022)

- Model: Linear (CBS/CW/Fox Nation), subscription (Paramount+), and free FAST (RidePass on Roku, Pluto TV, Sling, Fubo, and others) running simultaneously

Key Takeaways

Most diversified: From this set, PBR Team Series has the strongest and most diversified go-to-market. Linear (CBS/CW/Fox Nation), Paramount+ subscription, and RidePass FAST. Similarly, LOVB has ESPN linear, USA Network on Cable, Victory+ free, and ESPN+ subscription.

Neutral: TGL has the behemoth in ESPN but does not have a free or subscription streaming complement. PWHL has underdeveloped US national media rights with regional RSNs plus YouTube free distribution and no underlying subscription offering. While Unrivaled has a solid start with TNT/TruTV plus HBO Max, the revenue base and reach is narrower than PBR or LOVB.

Weaker: USL Super League is early but arguably on the weaker side of things with Peacock as the exclusive home of every match (more on Peacock soon). It is obviously missing the free distribution layer and does not have a linear broadcast complement.

Recent Industry Announcements

Versant Sports Portfolio: Versant, the Comcast cable network spinoff that began trading independently in January 2026, announced in November 2025 that “USA Sports” would be the unified brand and division name for its sports portfolio across USA Network, Golf Channel, and CNBC. The portfolio includes NASCAR, PGA Tour, Premier League, WWE, WNBA, USGA, LPGA Tour, and League One Volleyball (LOVB), totaling more than 10,000 hours of sports programming in 2026, approximately 1,000 of which are dedicated to women’s sports.

Scripps launches Scripps Sports Network: On March 24, 2026, E.W. Scripps launched Scripps Sports Network (SSN), a free, ad-supported streaming (FAST) channel distributed across Roku, Samsung TV Plus, LG Channels, Amazon Prime Video, Google TV, Xumo Play, and others. The channel is built around women’s sports, with 100+ live events planned for 2026 including PWHL (10 regular season games plus Walter Cup Finals), NWSL (59 games), and Major League Volleyball (12 games). It also carries 100+ hours of WNBA encore programming and original series. State Farm signed on as the founding advertising partner.

YouTube: In early April, YouTube announced new features for its TV (living room) experience, including Stations: YouTube’s entry into FAST. Creators can now launch 24/7 linear streams of their content without complex or costly setup, giving viewers an always-on channel experience similar to traditional TV.

Samsung and Roku: According to new data from Parks Associates (April 24, 2026), Roku and Samsung together account for 51% of primary connected TV devices in American homes — Roku’s OS leads at 28%, Samsung’s Tizen OS sits at 23%. Their dominance comes from three overlapping advantages: hardware diversity across price points, OS licensing (Roku licenses to Hisense, Sharp, and TCL; Samsung began licensing Tizen to other manufacturers in 2022), and built-in free streaming, including The Roku Channel and Samsung TV Plus. The Roku Channel alone accounted for nearly 3% of all TV viewed in February per Nielsen’s Gauge report, more than Paramount+ or HBO Max. Samsung TV Plus had 88 million monthly active users in 2025. Roku separately announced it had crossed 100 million global streaming households in mid-April 2026.

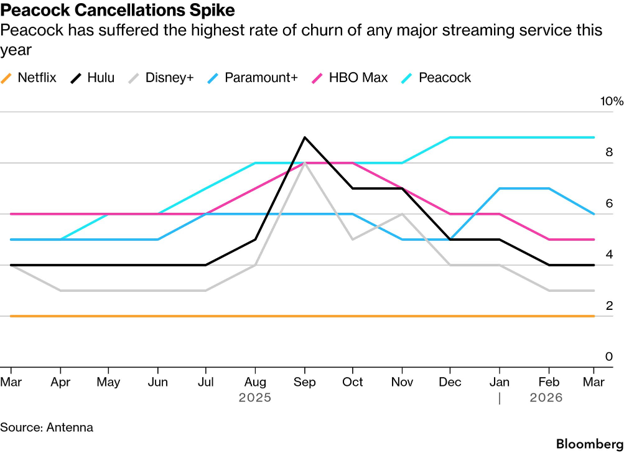

Peacock: As Lucas Shaw covered in an April 2026 weekly newsletter, Comcast has been operating Peacock for over six years and during that time has lost more than $11BN! While Peacock represented 3% of US TV viewing in February and has 46MM subscribers, per Antenna its churn rate of 9% is last among all of the major streaming services.

Where Do We Go From Here?

As mentioned earlier, the jagged frontier of Live Sports exists due to challenging economics, sub-optimal fan discovery, fragmentation across distribution and business models, difficulties retaining customers, and increasing competition for share of time spent (and willingness for fans to spend the time to watch an entire sporting event).

While ESPN remains the behemoth, there are strains participating in the ESPN ecosystem for non-tier 1 sports, especially for emerging leagues, as ESPN does not currently offer a free, ad supported channel. Further, ESPN+ has a wide array of content that can be difficult to find, will not necessarily be surfaced intuitively and timely and, especially if it’s a long tail property in ESPN’s live sports catalog, will receive no marketing or ancillary content supporting it.

And while Peacock is a DTC subscription offering, including availability in Prime Video Channels, the service continues to burn substantial cash 6 years in and it’s highly unlikely that a niche audience for an emerging sports league will ultimately move the needle for the service.

Last, I see Samsung, Roku, and YouTube’s news all as significant positives for all content creators and IP owners, including new and emergent sports leagues. However, I do not believe that these leagues can become self-sustainable on a free-only model. The audiences are not large enough and do not scale to the necessary levels on a stand-alone basis, due to lack of overlap audiences, to drive enough value to be the primary revenue source. Further, a free only offering prevents the free to subscribe flywheel and eliminates the subscription revenue potential from avid fans and future converts.

In Part 2 of this post, I’ll share an overarching framework that I believe allows emerging sports leagues to break through the stasis of the current jagged frontier for Live Sports. While this framework and proposed “Super App” approach may not resolve this situation in its entirety, if executed by well funded investors and experienced operators, it should be very possible to move the jagged frontier out much, much further.