Note: diagrams for the economic model and the structural workflow for the Super App can be found in the Appendix.

As covered in part 1 of this series, the jagged frontier for live sports exists for the following reasons:

- Economics: advertising only/advertising mostly or subscription only/subscription mostly business models are likely not the path to profitable longevity,

- Discovery: customer discovery remains a challenge, even when leagues are available on the largest TV platforms out there, including Roku and Samsung,

- Fragmentation: a customer pain point for every league, from the NFL and NBA down to college sports and below,

- Customer retention: for subscription-based services, churn is an ever-present challenge, that arguably becomes more and more challenging as the proliferation of customer options continues, and

- Engagement share: Competition for engagement and time spent, when you’re competing against behemoths like Netflix, YouTube, and Meta, has never been more challenging and will only get more competitive.

Recent Industry Announcements

Versant Sports Portfolio: Versant, the Comcast cable network spinoff that began trading independently in January 2026, announced in November 2025 that “USA Sports” would be the unified brand and division name for its sports portfolio across USA Network, Golf Channel, and CNBC. The portfolio includes NASCAR, PGA Tour, Premier League, WWE, WNBA, USGA, LPGA Tour, and League One Volleyball (LOVB), totaling more than 10,000 hours of sports programming in 2026, approximately 1,000 of which are dedicated to women’s sports.

Scripps launches Scripps Sports Network: On March 24, 2026, E.W. Scripps launched Scripps Sports Network (SSN), a free, ad-supported streaming (FAST) channel distributed across Roku, Samsung TV Plus, LG Channels, Amazon Prime Video, Google TV, Xumo Play, and others. The channel is built around women’s sports, with 100+ live events planned for 2026 including PWHL (10 regular season games plus Walter Cup Finals), NWSL (59 games), and Major League Volleyball (12 games). It also carries 100+ hours of WNBA encore programming and original series. State Farm signed on as the founding advertising partner.

CW partners with ESPN and Roku: The CW, which has built a live sports portfolio of roughly 800 annual hours over the past three years, including ACC, Pac-12, and Mountain West college football and basketball, NASCAR, WWE NXT, PBR, PBA, and AVP, announced dual streaming partnerships in April 2026. Its sports programming will stream exclusively on ESPN Unlimited, while its entertainment programming will appear on The Roku Channel the day after the linear premiere. The deals are revenue-sharing arrangements. Rather than launching its own DTC product, The CW chose to partner with established streaming platforms, with CW president Brad Schwartz noting the network concluded “the world does not need another direct-to-consumer product.”

Key takeaways

Versant: the USA sports cable channel arguably has low utility for emerging leagues. Legacy media distribution primarily focused on these is likely not a path to reaching and winning over a younger audience. Splitting league inventory, particularly on legacy media cable networks, also makes it challenging to maximize value due to inconsistent customer discovery and requiring multiple destinations to follow a team/season.

Scripps: The Scripps launch is less attractive for emerging leagues as a solely advertising model will be challenging. There’s also no DTC offering as part of its go-to-market. However, Scripps may end up partnering with ESPN as CW did (see #3). This also creates a split hodgepodge for PWHL (10 regular season games plus Walter Cup Finals), as one example.

CW: same issues as Versant in terms of legacy media distribution. Their live event inventory that does not air on the CW will go into the massive catalog of long tail sports within the ESPN+ portfolio without dedicated marketing, supporting content, or personalization efforts. Re Roku, at minimum it seems to be a stretch for customers to want to watch live events the day after they air on Roku.

Framework for building the most compelling and scalable option for Tier 2+ live sports

Focus is on new and emergent leagues that own IP and building a DTC Super App.

1. Economic model.

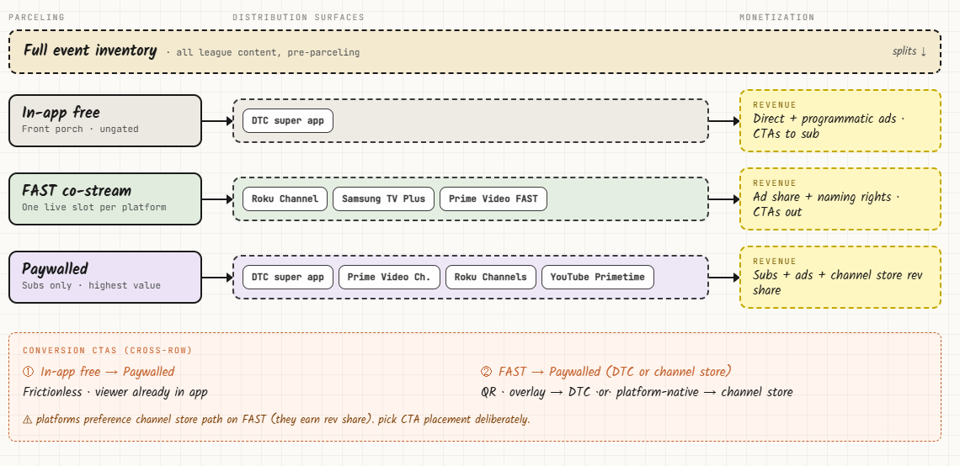

First we want to identify the total addressable market across all of the distribution channels we’ll work backwards from. To capture all of the potential value, we would create a Super App that houses all inventory for league partners, including paywalled subscription only live events (DTC and Channel Stores), live events in front of the paywall on Super App platform, and live events on FAST channels, e.g., Game of the Week, airing on channels such as Samsung TV+ and the Roku Channel.

Summary of the distribution channels:

- Free live event streams running on Super App DTC platform.

- This is for all of the inventory that is outside of DTC subscription and FAST co-stream programming highlighted below.

- Monetizes via revenue share on programmatic and direct ads.

- Drives awareness/CTAs for DTC subscription during live streams.

- FAST co-streams on Samsung TV Plus, The Roku Channel, Prime Video (PV).

- Co-stream or featured live streams of events (only one slot available at a time) on The Roku Channel et al.

- Naming rights, e.g., Game of the Week on Roku.

- Monetizes via revenue share on ads and naming rights, etc.

- Drives awareness/CTAs for DTC subscription during live streams.

- Co-stream or featured live streams of events (only one slot available at a time) on The Roku Channel et al.

- YouTube (YT).

- Co-stream to YouTube for identified FAST inventory.

- Drives awareness/CTAs for DTC subscription during live streams.

- DTC subscription, including daily, weekly, monthly, yearly, and bundling.

- Direct/programmatic advertising within the live event streams.

- Provide extra, value-add feature set relative to standard app that’s available in Channel Stores (e below).

- This is similar to the Tennis Channel’s model.

- Monetizes via DTC subscription.

- Channel Stores.

- Prime Video Channels.

- YouTube Primetime Channels.

- Monetizes via subscription revenue share.

- YouTube TV (YTTV).

- To the extent that it can secure distribution on YTTV, effectively the same offering as what’s on The Roku Channel, should do it; could even be within YouTube TV Sports rather than on the basic tier.

- Monetizes via affiliate fee and/or ad revenue share (if forego affiliate fee).

2. Programming strategy.

Programming strategy will be focused on maximizing value through broadening awareness and audience reach, driving revenue streams, including subscription and advertising, delineating between demand capture and demand generation strategies, and executing customer acquisition and customer retention that improves scale and operating leverage over time.

Key decisions include:

- What inventory goes in front of the paywall on the Super App?

- What inventory goes on dedicated off platform FAST channels?

- One example of this strategy would be having the first 2 of 5 days of a live event in front of the paywall, co-streamed on Prime Video, The Roku Channel, Samsung TV Plus et al.

- What inventory goes on the Subscription tier?

- We will then build self-reinforcing and learning mechanisms to improve this strategy over time via 1P and 3P data and Customer 360 data platform.

3. Executing off platform FAST channels.

- Samsung TV Plus and The Roku Channel are core focuses with Prime Video and YouTube as additional levers.

- Focus on the key areas of discoverability, including Sports Zones (Roku), search, and placement at the top of the homescreen.

- Dedicated sections, such as Roku’s coverage of the Olympics, are ideal, but unlikely as that model has proven tightly bespoke for Roku.

- Place QR code in FAST streams during live events to drive customers to subscription.

- This will vary by platform, but generally PV, YT, and Roku will want subscriptions driven to their Channel Stores where they extract a toll.

- Where we have discretion, we’ll decide how to delineate between Channel Store and DTC CTAs.

4. Executing CTV Apps.

- Living room (CTV) apps are most critical to success.

- While mobile engagement is important, people largely snack on this format and therefore monetizes at a lower rate.

- Will likely need to invest in “vertical video” to make this format most successful.

- Owl & Co is one of the industry thought leaders on vertical video. The sports content that likely translates best here includes “behind the scenes”, practice rounds, news show clips, video podcasts, and in and post-game highlights.

- Roku, Fire TV, Google TV, and Samsung are the focus, and then you pick between LG/VIZIO/Apple TV.

- Data clean room (DCR).

- Can set this up with Snowflake, for example, along with a data sharing agreement with Samsung and others.

- Run promotional campaigns and be able to determine impressions, click through rate from Samsung, and conversions through paid data in Super App’s payment logs — better visibility into ROAS than on social media.

- Identify customers who are acquired via CTV campaigns.

- Can also create look-a-like audiences leveraging the DCR to identify additional customers via demand generation (“you may also like…”).

5. Executing Channel Stores.

- The Channel Stores to focus on are 1) PV Channels, 2) Roku Channels, and to a lesser extent, 3) YouTube Primetime Channels.

- #3 would become a larger focus as YT drives more awareness and interest in this offering.

- While arguably lower friction to acquire new subscription customers, the tradeoff is that the channel store will take a revenue share cut of the revenue and often require a 7-day free trial with only a monthly subscription option.

- SKUs must also be at parity with off-platform DTC SKUs, including 1) pricing parity, 2) content parity, and 3) entitlement parity.

- While you could argue that it might be better to bypass Channel Stores through CTAs in FAST live streams, the distributors will not support this and will be much better partners if they have this flywheel within their ecosystem.

- Channel Stores are “full ingest model” and off platform DTC can be differentiated with additional features that the Channel Store app does not/cannot provide.

- Note: this is the model that the Tennis Channel follows as one example.

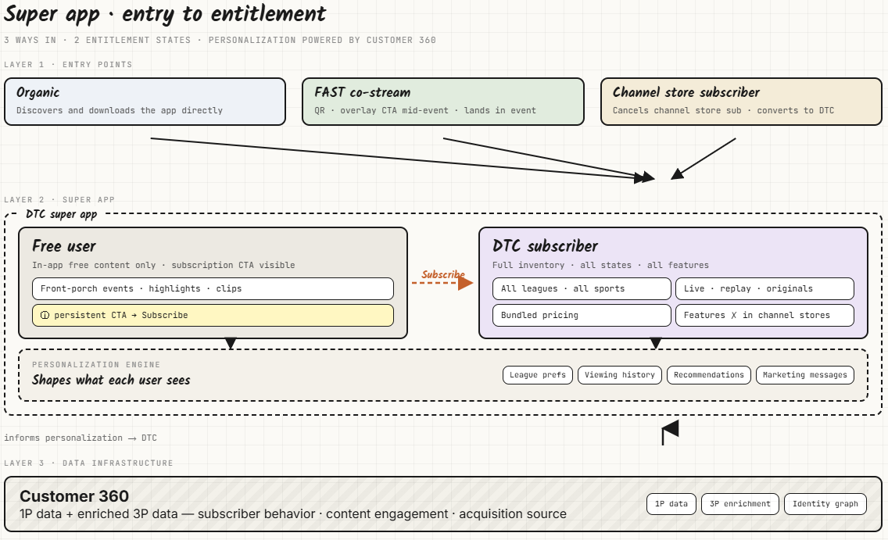

6. One Super App that provides entitlement and bundled discounts.

- Evergent or Cleeng as the possible entitlement layer.

- Establish subscription business models.

- Monthly.

- Yearly.

- Weekend.

- [Maybe] PPV.

- [Maybe] Daily.

- Provide access to all available leagues/sports at once.

- Gating is performed based on what is available:

- Off platform FAST,

- Outside DTC Super App’s paywall as a free live stream, and

- Behind the paywall on DTC Super App (and Channel Store apps).

- Find customer overlap interest for leagues and look to promote other leagues customers may like to drive higher retention.

- The app must be highly personalizable. The Super App should feel purpose built for the customer and that it focuses on their 1 to n sports and is not unnecessarily distracting with other content/leagues.

- Marketing and ancillary content scale across the leagues, and the data engine and agentic workflows are turbocharged by additional leagues that are added and finding lookalike audiences in CTV ecosystems.

- Gating is performed based on what is available:

7. Customer 360 for personalizing content and programming strategies, and marketing, including acquisition, retention, and upsell.

- 1P data, enriched with select 3P data, is a competitive advantage for the Super App.

- Content evaluation engine.

- Find look-a-like audiences for different sports.

- Target marketing.

- Segment audiences based on 100s of attributes logged in Customer 360 table.

8. Build agentic-based forecasting engine on 1P and 3P data for demand forecasting, programming strategies, and multi-year planning, among others.

- Complementary potential options:

Likely Partners/Tech Stack

- Snowflake or Databricks.

- Growthloop.

- Evergent or Cleeng.

- Claude for Enterprise.

- Amagi or Frequency for FAST delivery.

- Accedo for CTV development.

- TBC for Super App streaming technology.

- Viewlift acquired by DAZN.

- Kiswe is a potential partner.

Incumbent Summary

1. DAZN.

DAZN is a large-scale, primarily international company that has billions in revenue but has also continued to generate billions in free cash flow losses. Recently acquired ViewLift, which is compelling, but DAZN’s focus seemingly remains on Tier 1 rights; historically has included the rights for US tier 1 rights in international markets. Appears to also be in a likely long drawn battle with MLB teams and similar concerning the material discounts to teams’ local rights revenue relative to what they used to receive via the RSN model.

2. Kiswe.

Kiswe is an award-winning streaming technology company with proven experience powering DTC platforms for professional sports organizations including the Utah Jazz, Phoenix Suns, and New Orleans Pelicans. Recently selected as the technology partner for the Mountain West Conference’s new subscription streaming app, launching July 2026, covering 1,000+ live events annually across all 21 conference sports. This deal is a credible proof point for Kiswe’s ability to operate at conference scale, but there are some potential structural flaws:

- It fragments the DTC experience rather than consolidating it into a super app (school sites and Mountain West site),

- The conference retains linear distribution across CBS, FOX, and The CW at a time when linear viewership no longer reaches the student body demo.

- The inventory that flows to ESPN Unlimited via The CW deal risks low discovery on a platform that has limited incentive to market emerging league content.

3. ESPN.

ESPN launched its long-anticipated standalone streaming service in August 2025 at $30 per month, making it one of the most expensive streaming products on the market. Disney has been quiet about subscriber uptake since launch. On its recent earnings calls, Disney has made limited mention about ESPN’s streaming initiatives and ESPN Unlimited. For emergent leagues, ESPN Unlimited represents reach but building and maintaining the customer relationship is left entirely to the fractured rights holders who have limited visibility without 1P data access. Rights partners have no subscriber data access, make no pricing decisions, and no ability to build a direct fan connection.

The Super App strategy proposed here diverges from the ESPN model: own the subscriber, own the data, own the economics.

Appendix

Economic Model

How the Super App Works